CAPEX networks CAPEX

A modern AI datacenter is not a collection of individual servers, it is a distributed supercomputer where thousands of GPUs must act as a single unified compute fabric. Training a large frontier model like GPT-4 required roughly 10,000 GPUs operating in tight coordination, exchanging weights, gradients and activations continuously. The moment those GPUs cannot communicate fast enough, compute sits idle and the entire cluster underperforms.

Network chips solve this problem: they move data between GPUs, between servers, between racks, and between datacenters at the speeds required to keep compute utilization high. As GPU performance has compounded by 1,000x over eight years, the networking layer has had to keep pace or become the bottleneck. Bandwidth demand inside AI clusters, in fact, scales faster than compute itself, which makes networking silicon one of the most structurally critical layers in the entire AI infrastructure stack.

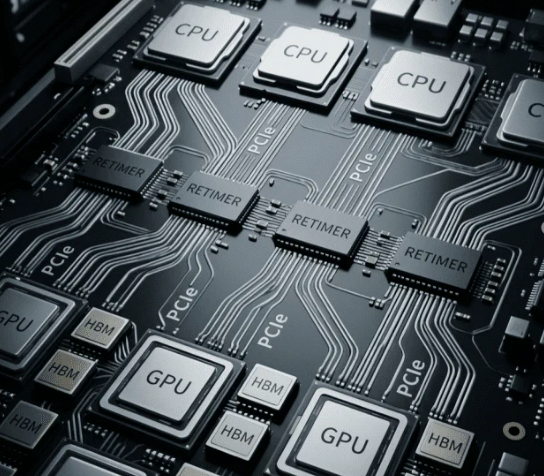

The networking layer inside an AI datacenter is made up of several distinct chip categories, each solving a different part of the connectivity problem. Switching chips sit at the core of the network fabric, directing traffic between servers and racks at terabit-scale bandwidth BROADCOM's Tomahawk 6, capable of 102.4 Tbps, is the current state of the art. Optical DSPs (Digital Signal Processors) encode and decode high-speed optical signals inside the fiber modules that connect servers across longer distances within the datacenter, where copper no longer works reliably at 400G and 800G speeds. Active Electrical Cable (AEC) chips CREDO's core product handle shorter-reach connections within a rack, replacing traditional passive copper cables with intelligent signal conditioning that extends reach and improves power efficiency. PCIe retimers regenerate the electrical signal between a CPU and its attached GPUs inside a server chassis; as AI servers pack more GPUs per box, signal integrity degrades and retimers become mandatory components in every build. Finally, CXL (Compute Express Link) memory controllers enable shared memory access across multiple CPUs and GPUs a capability becoming increasingly important as model sizes exceed what any single processor can hold.

BROADCOM is the undisputed anchor of datacenter networking. Its Tomahawk switching chips are the backbone of the Ethernet fabric used in the largest AI clusters, and its custom ASIC business designing purpose-built AI accelerators for GOOGLE, META, ANTHROPIC and OPENAI has become a second engine of extraordinary growth.

MARVELL sits between merchant silicon and custom ASIC design. It leads in optical DSPs the chips inside the fiber modules that physically move data at 400G and 800G speeds and co-designs custom accelerators with hyperscalers, most notably co-designing TRAINIUM chips for AWS. NVIDIA itself invested $2B into MARVELL and folded its custom ASIC roadmap into the NVLink Fusion ecosystem, an unusually strong signal of strategic alignment.

CREDO is the pure-play AEC specialist. Its ZeroFlap active cable technology dominates short-reach intra-rack connectivity, and its PAM4 DSPs are increasingly embedded in 800G deployments. The upcoming transition to 1.6T connectivity in late 2026/2027 represents a major step-up in average selling prices, making CREDO one of the clearest velocity plays in the networking stack.

ASTERA LABS occupies a more specialized but highly defensible niche: PCIe retimers and CXL memory controllers. Its Aries PCIe retimer is the dominant component in AI server builds requiring signal regeneration between CPUs and GPU arrays required in virtually every high-density AI server shipping today.

The networking layer is arguably the most structurally under appreciated part of the AI infrastructure trade, precisely because it lacks the narrative clarity of GPUs yet bandwidth demand scales faster than compute, meaning every GPU generation upgrade pulls an immediate and proportional demand upgrade for networking silicon.

BROADCOM is the highest-conviction, lowest-volatility expression of this theme. Its dual engine custom ASICs plus switching chips gives it exposure to both the compute and connectivity layers, with a $73B backlog providing multi-year revenue visibility. The VMware software business adds a high-margin, recurring revenue floor that allows § to sustain aggressive R&D investment without balance sheet risk. It is, in every sense, the primary architect of the custom silicon and networking infrastructure underpinning the AI supercycle. BROADCOM delivered another exceptional quarter, with Q2 revenues reaching a record $22.2B (+48% YoY) and adjusted EBITDA margins expanding to 69%. The AI semiconductor business is the standout, with Q2 AI revenue doubling to $10.8B and Q3 guidance projecting over 200% YoY AI growth, implying total Q3 revenue of $29.4B (+84% YoY). Valuation looks attractive on a forward PEG of just 0.68, and recent share price weakness appears to reflect short-term margin noise rather than any deterioration in the underlying business. However, customer concentration is a material overhang: GOOGLE's TPU program is expected to reduce its reliance on BROADCOM's custom silicon over time, potentially representing a $15–25B headwind to FY28 revenue versus a scenario where no second-source emerges. Neither risk is existential given the breadth of BROADCOM's order pipeline and its $73B backlog, but they are real valuation constraints that investors should weigh carefully against the undeniably strong near-term execution.

MARVELL is the most compelling risk/reward in the large-cap networking space. The NVIDIA strategic investment validates its optical DSP positioning, its custom ASIC wins with AWS are ramping. It offers BROADCOM-like structural exposure at a valuation that has not yet re-rated to reflect the magnitude of its AI design wins.The real structural catalyst for MARVELL was not Jensen Huang's headline trillion-dollar comment on June 2, it was the $5B FY27 guide raise disclosed six days earlier. MARVELL now guides to approximately $11.5B in FY27 revenue (+40% YoY) and $16.5B in FY28 (+45%), with interconnect growth guidance raised from 50% to over 70% YoY. What makes MARVELL's positioning genuinely differentiated is its dual engine: most AI infrastructure names benefit from either custom silicon or optical interconnect, MARVELL gets both. Custom ASIC wins spanning AWS Trainium, MICROSOFT Maia, META's DPU, and GOOGLE Axion provide diversified hyperscaler exposure that de-risks the revenue profile from any single customer cycle, while the optical interconnect business benefits directly from the insatiable bandwidth demand that scales faster than compute itself. Data center now represents 76% of total revenues, and custom ASIC revenue is projected to double in FY28. The newly introduced Teralynx T100 switch further expands MARVELL's addressable market into AI fabric switching, adding another growth vector beyond its core DSP and ASIC businesses. The key tension is valuation. At 68x forward P/E, MARVELL is priced for continued flawless execution, leaving limited margin for error. Gross margin softness persists despite top-line and EPS beats, and at these multiples any guidance disappointment would be punished severely. That said, the combination of diversified hyperscaler design wins, accelerating optics demand, and a structurally raised multi-year revenue outlook justifies a positive outlook with the caveat that position sizing should reflect the valuation premium embedded in the stock.

CREDO is the highest-growth, highest-volatility name. Its AEC technology has strong customer stickiness, gross margins above 60% are exceptional for a hardware company, and the 1.6T transition is a discrete, time-stamped catalyst for a significant ASP step-up. The stock pulled back sharply from its February 2026 highs after guidance suggested normalizing growth rates a classic reset in a priced-for-perfection name which likely creates a more attractive entry point ahead of the 1.6T ramp. CREDO delivered a standout FY2026, with Q4 revenue surging 157% YoY to $437M, 68.3% gross margins and 51.9% net margins that speak to genuine pricing power rather than volume-driven growth. Guidance points to continued triple-digit growth with improving operating leverage, while the forward PEG of 0.98 makes CREDO one of the few high-growth AI infrastructure names that has not yet been fully re-rated by the market. The strategic picture is increasingly compelling. CREDO's core AEC business benefits directly from the insatiable bandwidth demand driving hyperscaler buildouts, and the DustPhotonics acquisition meaningfully strengthens its silicon photonics capabilities, expanding its 800G and 1.6T optical portfolio at precisely the moment the industry is transitioning toward facility-wide optical architectures. Critically, CREDO is not a one-dimensional connectivity play its vertically integrated copper and optical portfolio positions it across both scale-up (GPU-to-GPU within a cluster) and scale-out (cluster-to-cluster across the datacenter) architectures, giving it exposure to every layer of the AI networking fabric. The upcoming Weaver memory fanout gearbox chiplet adds yet another dimension, creating a direct path to monetize the AI memory supercycle that MICRON's latest earnings commentary reinforced — tightening constraints in bandwidth, capacity, latency and power efficiency translate directly into demand for faster, lower-power connectivity solutions. The primary risk is customer concentration. A meaningful share of CREDO's revenue remains tied to a small number of hyperscalers, and integrating DustPhotonics while simultaneously scaling advanced optical products introduces execution complexity. At current levels these risks appear well-compensated, but they are real constraints on the multiple that the stock can sustainably command.

ASTERA LABS has the highest gross margin profile in the group (above 75%) and a genuinely defensible moat in PCIe retimers, where it holds dominant market share in a component that ships in every AI server. The Scorpio switching entry is a meaningful TAM expansion that the market has not yet fully priced. ASTERA LABS delivered another strong quarter, with Q1 revenue up 93% YoY and gross profit growing 97% YoY a combination that reflects both the strength of hyperscaler AI capex tailwinds and the company's ability to expand margins as it scales. As a pure-play on AI infrastructure connectivity, ASTERA LABS occupies a genuinely differentiated position: its Aries PCIe retimers are embedded in virtually every high-density AI server shipping today, while Scorpio, its AI fabric switch line is emerging as the company's next major growth engine and is expected to become its largest product line by 2026, anchored by a $6.5B AMAZON warrant agreement that provides unusual revenue visibility for a company of its size. The Leo CXL memory controller and Taurus AEC product lines round out a portfolio that touches every major connectivity layer inside an AI datacenter. The tension, as with MARVELL, is entirely in the valuation. At 196x P/E and 301x EV/EBITDA, ASTERA LABS is priced not just for perfection but for a sustained multi-year compounding trajectory that leaves essentially no room for execution missteps. Customer concentration is a real risk the AMAZON warrant structure, while a validation of Scorpio's technical merit, also means that any deterioration in that relationship would have outsized revenue consequences. Competitive pressure in the AEC segment from CREDO and MARVELL could constrain Taurus growth, and BROADCOM's scale and customer relationships represent a structural overhang in switching. ASTERA LABS is a high-quality business compounding at an exceptional rate but at current multiples, it is a stock where the entry point matters enormously.

Cautious investors should focus on BROADCOM while growth ones should have a combination of MARVELL and CREDO in the networks space. I would pass on ASTERA LABS for now.